Understanding Payment Processing Fees: A Complete Guide for Merchants

Sarah Mitchell

30 March 2026

Understanding Payment Processing Fees: A Complete Guide for Merchants

Introduction

Every time a customer swipes their card or clicks “buy now” on your website, a complex financial transaction unfolds behind the scenes. While you see the sale, what you might not fully grasp is the intricate web of fees that quietly chip away at your revenue. Payment processing fees can significantly impact your bottom line, yet many merchants operate without a clear understanding of these costs.

In today’s competitive marketplace, understanding payment processing fees isn’t just beneficial—it’s essential for business survival. These fees typically range from 1.5% to 3.5% of each transaction, which means a business processing $100,000 monthly could pay between $1,500 and $3,500 in fees alone. That’s $18,000 to $42,000 annually!

This comprehensive guide will demystify the complex world of payment processing fees, helping you make informed decisions that can save your business thousands of dollars each year. From interchange rates to assessment fees, we’ll break down every component so you can optimize your payment strategy and maximize profitability.

Understanding the Payment Processing Ecosystem

The Key Players in Every Transaction

When a customer makes a purchase, multiple parties are involved in processing that payment, and each takes their share:

- Issuing Bank: The customer’s bank that issued the credit card

- Acquiring Bank: Your merchant bank that processes payments

- Card Networks: Visa, Mastercard, American Express, Discover

- Payment Processor: The company that facilitates the transaction

- Payment Gateway: The technology that securely transmits payment data

- The full amount is initially authorized

- Various fees are deducted during settlement

- You receive the net amount (typically $96.50-$98.50)

- The difference represents the total processing costs

- Card type: Rewards cards cost more than basic cards

- Transaction method: Card-present vs. card-not-present

- Business type: Some industries qualify for lower rates

- Transaction size: Larger transactions may have different fee structures

- Visa/Mastercard debit (card-present): 0.05% + $0.21

- Visa/Mastercard credit (card-present): 1.51% + $0.10

- Visa/Mastercard credit (online): 1.80% + $0.10

- Premium rewards cards: 2.30% + $0.10 or higher

- Visa: 0.14% of transaction volume

- Mastercard: 0.13% of transaction volume

- American Express: Varies, typically higher

- Discover: 0.13% of transaction volume

- Fixed markup: A set percentage added to interchange

- Per-transaction fees: Fixed amount per transaction

- Monthly fees: Account maintenance, statement fees

- Incidental fees: Chargeback fees, PCI compliance fees

- Interchange rate + processor markup

- Example: 1.80% + 0.30% = 2.10% total

- Benefits: Complete transparency, typically lowest cost

- Best for: Businesses processing $5,000+ monthly

- Qualified: Lowest rate (basic cards, optimal conditions)

- Mid-qualified: Medium rate (rewards cards, suboptimal conditions)

- Non-qualified: Highest rate (premium cards, worst conditions)

- Card-present: Typically 2.6% to 2.9%

- Card-not-present: Typically 2.9% to 3.5%

- Benefits: Predictable, easy to understand

- Drawbacks: Usually more expensive for larger businesses

- Industry type: High-risk industries pay premium rates

- Processing history: New businesses often start with higher rates

- Chargeback ratio: High chargeback rates increase costs

- Credit score: Business and personal credit affect approval and rates

- Monthly minimum fees: Charged if you don’t meet processing thresholds

- Statement fees: $10-$25 monthly for detailed reporting

- PCI compliance fees: $5-$30 monthly for security compliance

- Annual fees: Some processors charge yearly account fees

- Authorization fees: $0.05-$0.15 per transaction attempt

- Batch fees: $0.10-$0.25 per daily settlement

- Voice authorization: $1-$3 for phone approvals

- International fees: 1-2% additional for foreign cards

- Chargeback fees: $15-$50 per disputed transaction

- Retrieval fees: $10-$25 for transaction inquiries

- NSF fees: $25-$35 for failed ACH transfers

- Early termination fees: $200-$500 for contract cancellation

- Promote debit card usage over credit cards

- Offer ACH/bank transfer discounts for large purchases

- Implement contactless payments to reduce processing time

- Ensure all required transaction data is captured

- Process transactions within 24 hours

- Use proper merchant category codes

- Maintain PCI compliance to avoid penalties

- Request interchange-plus pricing

- Negotiate lower markup rates

- Ask for volume discounts

- Eliminate unnecessary monthly fees

- Negotiate when your volume increases

- Review rates annually

- Use competitor quotes as leverage

- Consider switching if terms don’t improve

- Use EMV-capable terminals to reduce fraud

- Implement address verification (AVS) for online sales

- Use fraud detection tools to prevent chargebacks

- Ensure fast, reliable internet connections

- Batch process transactions daily

- Train staff on proper payment procedures

- Monitor and dispute incorrect fees promptly

- Maintain detailed transaction records

- Effective processing rate across all transaction types

- Monthly fees and minimums

- Setup and equipment costs

- Contract terms and cancellation policies

- 24/7 customer support availability

- Technical support quality

- Account management services

- Dispute resolution assistance

- Compatibility with your POS system

- E-commerce platform integration

- Mobile payment capabilities

- Reporting and analytics tools

- What is your exact markup over interchange rates?

- Are there any fees not mentioned in your standard pricing?

- What are your contract terms and cancellation policies?

- How do you handle rate increases?

- What support do you provide for chargebacks and disputes?

- Can you provide references from similar businesses?

- Adult entertainment: 4-8% processing rates

- Nutraceuticals: 3-6% due to chargeback risk

- Travel: Variable rates based on advance booking

- Subscription services: Higher rates due to recurring billing

- Negotiate volume-based pricing

- Avoid high monthly minimums

- Plan for rate changes during peak seasons

- Consider seasonal processor agreements

- Interchange rate regulations

- Data privacy requirements

- Open banking initiatives

- Cross-border payment regulations

- Transparency matters: Choose processors that clearly explain their fee structure

- Volume gives leverage: Higher processing volumes unlock better rates

- Technology investments pay off: Better systems reduce costs and improve security

- Regular reviews are essential: Payment processing is an ongoing optimization opportunity

- Audit your current processing costs: Calculate your effective rate across all transaction types

- Request quotes from 3-5 processors: Use our evaluation criteria to compare options

- Negotiate with your current processor: Armed with competitor quotes, push for better terms

- Implement optimization strategies: Focus on transaction qualification and cost reduction techniques

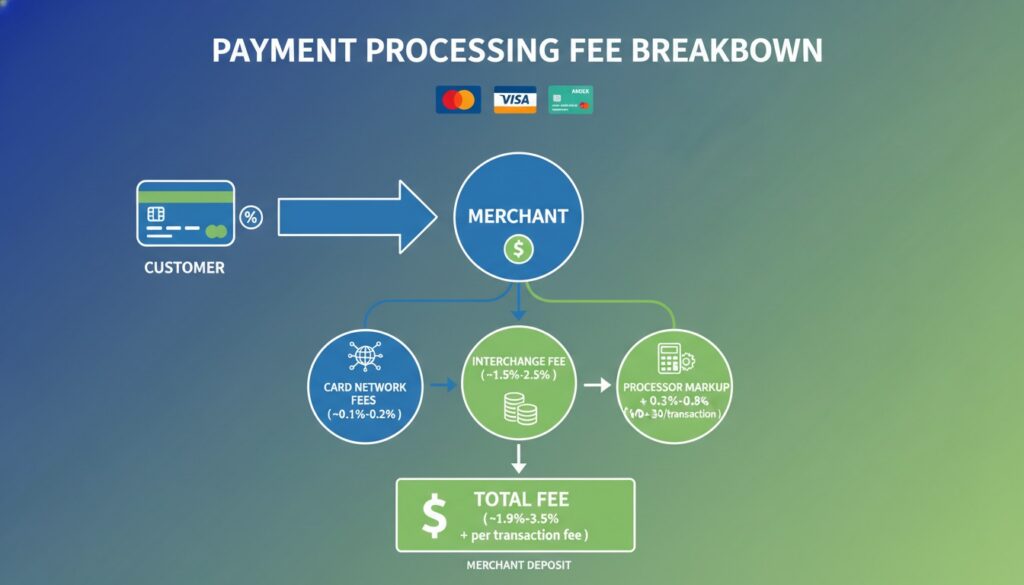

How Money Flows Through the System

Understanding the payment flow helps explain why fees exist. When a customer pays $100:

Pro Tip: The faster you want your money, the more you’ll typically pay in fees. Same-day funding often costs an additional 0.5% to 1%.

Breaking Down Payment Processing Fee Types

Interchange Fees: The Largest Component

Interchange fees are non-negotiable rates set by card networks and paid to issuing banks. These fees represent 70-80% of your total processing costs and vary based on:

Assessment Fees: Network Costs

Card networks charge assessment fees for using their payment rails:

Processor Markup: Where Competition Exists

This is where you have negotiating power. Processor markup includes:

Payment Processing Pricing Models Explained

Interchange-Plus Pricing: The Most Transparent

Interchange-plus pricing shows exactly what you’re paying:

Tiered Pricing: Simple but Often Expensive

Processors group transactions into tiers:

Flat-Rate Pricing: Predictable but Premium

Companies like Square and PayPal offer flat rates:

Factors That Impact Your Processing Fees

Transaction Characteristics

Card-Present vs. Card-Not-Present

Card-present transactions (chip, swipe, tap) have lower interchange rates because they’re more secure. Online and phone orders carry higher rates due to increased fraud risk.

Transaction Size and Frequency

Larger average transaction sizes often result in lower effective rates, while high-volume businesses can negotiate better terms.

Business Risk Factors

Seasonal and Volume Fluctuations

Processors may offer volume discounts or seasonal rate adjustments for businesses with predictable patterns.

Hidden Fees to Watch Out For

Monthly and Annual Fees

Transaction-Specific Fees

Penalty and Incidental Fees

Important: Always read the fine print. Some processors have dozens of potential fees that can add up quickly.

Strategies to Minimize Payment Processing Costs

Optimize Your Transaction Mix

Encourage Lower-Cost Payment Methods

Negotiate Better Terms

Leverage Your Processing Volume

Businesses processing over $10,000 monthly should negotiate custom rates:

Technology and Process Improvements

Invest in Better Payment Technology

Choosing the Right Payment Processor

Evaluation Criteria

Cost Structure Analysis

Don’t just compare advertised rates. Calculate total costs including:

Questions to Ask Potential Processors

Industry-Specific Considerations

High-Risk Industries

Some industries face higher processing costs:

Seasonal Businesses

Businesses with seasonal fluctuations should:

Future Trends in Payment Processing

Emerging Payment Methods

Digital Wallets and Mobile Payments

Apple Pay, Google Pay, and Samsung Pay often have similar rates to card-present transactions while offering enhanced security.

Cryptocurrency Integration

While still emerging, crypto payments can offer lower fees but come with volatility risks and regulatory considerations.

Buy Now, Pay Later (BNPL)

Services like Klarna and Afterpay charge merchants 2-8% but can increase conversion rates and average order values.

Regulatory Changes

Stay informed about:

Conclusion

Understanding payment processing fees is crucial for any business accepting electronic payments. While the fee structure may seem complex, breaking it down into its core components—interchange fees, assessment fees, and processor markup—makes it manageable.

The key takeaways for merchants are:

Remember, the cheapest option isn’t always the best. Consider the total cost of ownership, including support quality, technology capabilities, and contract flexibility when making your decision.

Take Action: Optimize Your Payment Processing Today

Don’t let payment processing fees eat away at your profits any longer. Start by:

Schedule your free payment processing audit now and start saving money on every transaction.